Tangible Property Exchange

Property other than real estate can be exchanged, such as construction equipment. The property exchanged must be held for investment or productive use in a business or trade and must be exchanged for property.

Construction Exchange

(also called Improvement Exchange or Build-To-Suit Exchange) A Construction Exchange allows an exchanger to use the proceeds from the sale of their relinquished property to build on or make improvements to their replacement properties.

Reverse Exchange

A Reverse Exchange allows the exchanger to first acquire their replacement property and then sell their current investment property at a later date. This is to the exchanger's advantage when their desired replacement property is available for purchase prior to the sale of their current investment property.

Delayed Exchange

In a Delayed Exchange, the exchanger relinquishes their current investment property and then acquires a replacement property at a later date. This is the most common type of exchange.

Simultaneous Exchange

In a Simultaneous Exchange, the exchanger relinquishes their current investment property and acquires their replacement property on the same day.

Types of Exchanges

Frequently Asked Questions

Why Exchange?

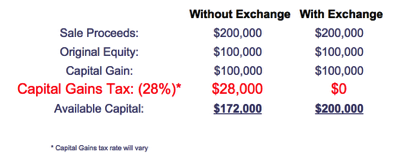

By deferring payment of capital gains tax, a property owner will have more capital available to acquire new investment property. This will allow the investor to purchase more expensive property and/or receive greater cash flow on an income producing investment.

An Example:

Types of property that qualify?

The IRS requires that the properties exchanged be of 'like-kind' and must be 'held for investment.' In general, any real property, other than one's primary residence, is considered to be 'held for investment.' For purposes of a 1031 Exchange, all real estate qualifies as 'like-kind.' For example, an office building may be exchanged for raw land, raw land may be exchanged for a rental property, etc.

What is the timing involved with an Exchange?

The exchanger has 45 calendar days from the close of escrow on the relinquished property to identify up to 3 replacement properties. The exchanger mus then acquire at least one of these properties within 180 calendar days from the close of escrow on the relinquished property. It is possible to identify and purchase more than 3 replacement properties, provided certain guidelines are followed.

Can the exchanger receive a portion of the sale proceeds?

Yes, the exchanger can receive a portion of the sale proceeds. This is referred to as 'boot.' However, this portion will be subject to capital gains tax. The remaining proceeds held in the Exchange are still tax-deferred.

Why is a Qualified Intermediary necessary?

The exchanger may not have 'constructive receipt' of the sale proceeds and therefore, the IRS requires the use of a Qualified Intermediary for all 1031 Exchange transactions. The Qualified Intermediary holds the funds on behalf of the exchanger. The funds are then released when new investment property is acquired.

What happens when the new investment property is sold?

When a real estate investor sells a property that was acquired in a 1031 Exchange, the deferred capital gains tax, as well as any new capital gains tax, will be due. However, the investor may enter into another 1031 Exchange and continue to defer payment of all capital gains tax.

Missouri Central Law, LLC

Address: 123 East Third Street, Cameron, MO 64429

Phone: 816-632-6679 Fax: 816-632-1114

Monday - Friday 9AM - 5PM ~ Saturday by appointment